MAGNA report: APAC ad market to grow by 8.5% in 2024

share on

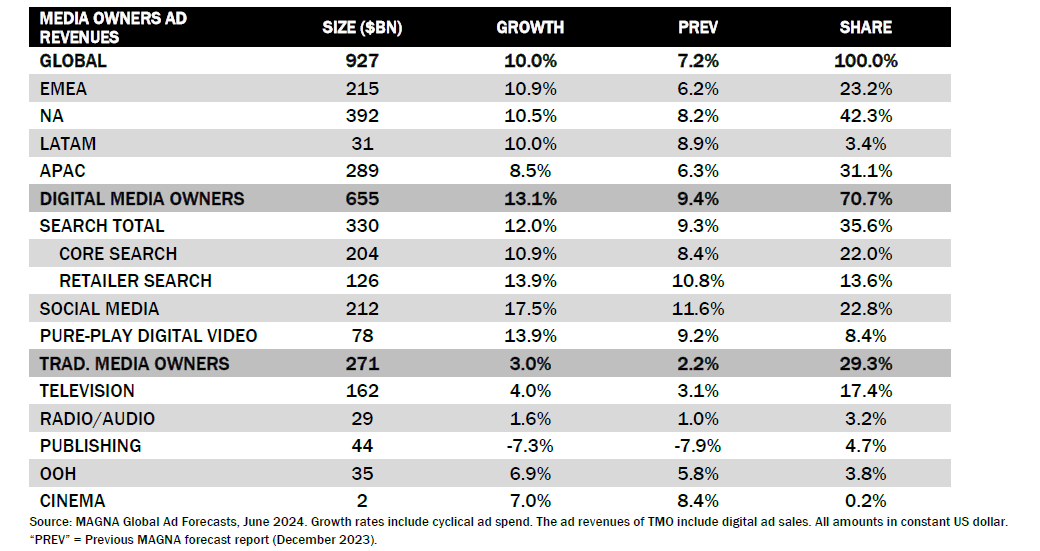

The APAC ad market will grow by 8.5% this year to reach US$289 billion, according to MAGNA's latest report.

This follows a +9.5% growth in 2023, when the market hit US$266 billion. The growth is taking place in a slightly slowing, but stable, economic environment where real GDP is expected to grow by 5.2% in 2024, according to the IMF.

This increase in growth is primarily driven by the tailwinds of sporting events – primarily the Paris Olympics. Meanwhile, the UEFA Euro 2024 tournament and other sporting events typically have only a minor impact in APAC markets, according to the report.

Inflation in APAC has continued to decline and while some economies are still seeing sustained price pressures, others are facing deflationary risks. Global disinflation and the prospect of monetary easing have increased the likelihood of a soft landing.

In 2024, the strongest growth in APAC is expected to come from Sri Lanka (+12%), India (+11.8%), and Japan (+11.8%). This represents a significant jump in growth for Japan, following 2023’s +5.6% growth rate. Growth in many traditionally mature markets is rebounding in 2024. APAC as a region is still dominated by China, which represents approximately half of total ad revenues. When combined with Japan, Australia, India, and South Korea, those five large markets represent 87% of total APAC revenues.

According to the report, digital advertising revenues are the driver of growth in APAC. Search remains the largest portion of digital advertising revenues and will represent US$103 billion in 2024. This is 47% of total digital advertising budgets.

Search advertising in APAC is substantially driven by retail media platforms, especially in China where Alibaba, JD.com, Pinduoduo, and Meituan all drive search advertising revenues. Core search is also spiking around the world as traditional search platforms such as Google and Baidu also see strong performance relative to recent results.

Furthermore, social media advertising revenues also remain strong in 2024. While social media was already surging ahead in 2023 in APAC (+19% growth to reach US$65 billion), growth will again be robust in 2024 (+15% to reach US$74 billion). This means social media budgets will represent 34% of total digital advertising budgets.

Both search and social media revenues are driven by mobile devices. Smartphones are not just the dominant way that most consumers access the internet; in many APAC markets they are the only way consumers access the internet. Many consumers skipped the desktop hardware generation and conduct their digital lives solely on their smartphones.

While in China, the report said consumers don’t just do shopping and communication on smartphones, but also banking, insurance, and many work functions. Because of this, 76% of total digital advertising revenues in APAC are on mobile devices.

The digital strength driving APAC advertising revenues will translate to continued share gains for digital advertising revenues in APAC. Digital revenues will represent 81% of total budgets in 2028, up from 76% of total advertising revenues in 2024.

Global advertising growth forecast

Looking from a global point of view, the advertising revenues of traditional media owners (TMO), including TV, radio, publishing, and out-of-home (OOH) media, are expected to reach US$272 billion in 2024, representing a 3% increase compared to 2023 when revenues declined by 4%.

The TMO ad sales are driven by a record number of cyclical events such as Paris Olympics and UEFA Euro 2024, as well as an 11% growth in TMO’s non-linear ad sales such as ad-supported streaming, digital audio, publishers’ digital ad sales, are now accounting for 25% of total TMO ad revenues.

Ad-supported streaming is taking off in 2024, as traditional TV players such as Disney+, Max and ITV Hub, as well as pure streaming players including Netflix and Amazon will generate at least US$18 billion this year (+16%).

Meanwhile, the advertising sales of digital pure players (DPP) offering search/ commerce, social, short-form video, static banners, and digital audio ad formats, will increase by 13% to reach US$655 billion. It is boosted by increased competition in eCommerce, the rise of retail media networks (US$146 billion this year), and better monetisation of short vertical videos in video apps and social media apps.

According to the report, keyword search remains the largest digital ad format, growing by 12% to reach US$330 billion this year. Social media owners such as Meta and TikTok accelerate (+18% to US$212bn), while short-form pure-play video platforms (e.g., YouTube, Twitch) grow by +14% to reach US$78 billion.

Automotive and CPG and FMCG brands will be among the fastest-growing ad spending verticals this year, while finance re-accelerates and government expands due to the many elections taking place this year.

Meanwhile, the retail industry will show moderate advertising activity overall, as an average between traditional brick-and-mortar brands slowing down from mature levels of marketing spending, and new eCommerce brands such as Temu and Shein developing their share of voice aggressively, according to the report.

The report has raised its 2024 ad revenue growth forecast upwards, due to a stronger-than-expected 12% increase in the global ad market during the first quarter of 2024, with global real GDP growth forecast at 3.2% and APAC GDP growth at 5.2%.

Don't miss: MAGNA report: Ad spend for 2023 and a breakdown of the mediums

Vincent Létang, EVP, global market research at MAGNA, and author of the report, said: “Based on MAGNA’s analysis of media companies' financial, advertising revenues were much stronger than expected in the first quarter of 2024. Coupled with some improvement in the macro-economic outlook, this leads us to increase our full-year global advertising growth forecast from +7.2% (December 2023 update) to +10%. All categories of media owners are faring better than expected so far this year, including traditional media owners and, specifically, television and premium long-form video."

Paul Waller, chief investment officer MAGNA APAC, said: "Despite economic uncertainties, the global and APAC advertising market continues to expand. With digital ad spend leading the charge and projected to reach unprecedented heights in the coming years. Now that inflation in commodity costs and consumer prices are under control, marketers are returning to previous levels of advertising budgets and taking advantage of the investment opportunities offered. With a heightened focus towards more targeted and data-driven marketing strategies."

Join us this coming 26 June for Content360 Hong Kong, a one-day-two-streams extravaganza under the theme of "Content that captivates". Get together with our fellow marketers to learn about AI in content creation, integration of content with commerce and cross-border targeting, and find the recipe for success within the content marketing world!

Related articles:

Study: SEA retail media network ad spend to hit US$4.7 billion by 2030

Survey: HK ad spend reaches HK$30.1bn in 2023

Study: 49% of marketers expect to increase ad spend on podcasts

share on

Free newsletter

Get the daily lowdown on Asia's top marketing stories.

We break down the big and messy topics of the day so you're updated on the most important developments in Asia's marketing development – for free.

subscribe now open in new window